2023 Q3 Tax Calendar: Key Deadlines for Businesses and Other Employers

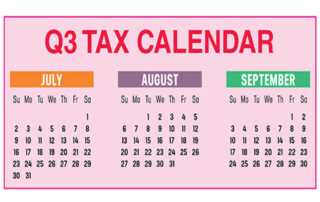

Here are some of the key tax-related deadlines affecting businesses and other employers during the third quarter of 2023. Keep in mind that this list isn’t all-inclusive, […]

Here are some of the key tax-related deadlines affecting businesses and other employers during the third quarter of 2023. Keep in mind that this list isn’t all-inclusive, […]

Expanding operations into foreign countries can help U.S. businesses reduce labor and operating costs. It can also provide them with access to new markets and potentially higher […]

If you’re age 65 and older and have basic Medicare insurance, you may need to pay additional premiums to get the level of […]

Your business may be able to claim big first-year depreciation tax deductions for eligible real estate expenditures rather than depreciate them over several […]

There are many types of professional practices. Examples include medical, architecture, engineering, accounting, advertising, design and law. From a business valuation perspective, it’s important to recognize the […]

As posted to the Climate One YouTube page on 7/17/23

Run Time 58 minutes, 47 seconds (

High-income taxpayers face a regular income tax rate of 35% or 37%. And they may also have to pay a 3.8% net investment income tax (NIIT) that’s imposed in […]

If you and your employees are traveling for business this summer, there are a number of considerations to keep in mind. Under tax […]

If you’re considering buying a company, fraud may be the last thing on your mind. Unfortunately, you can’t afford to ignore the possibility […]

You may think you don’t need to make any estate planning moves because of the generous federal estate tax exemption of $12.92 million for 2023 (effectively $25.84 […]