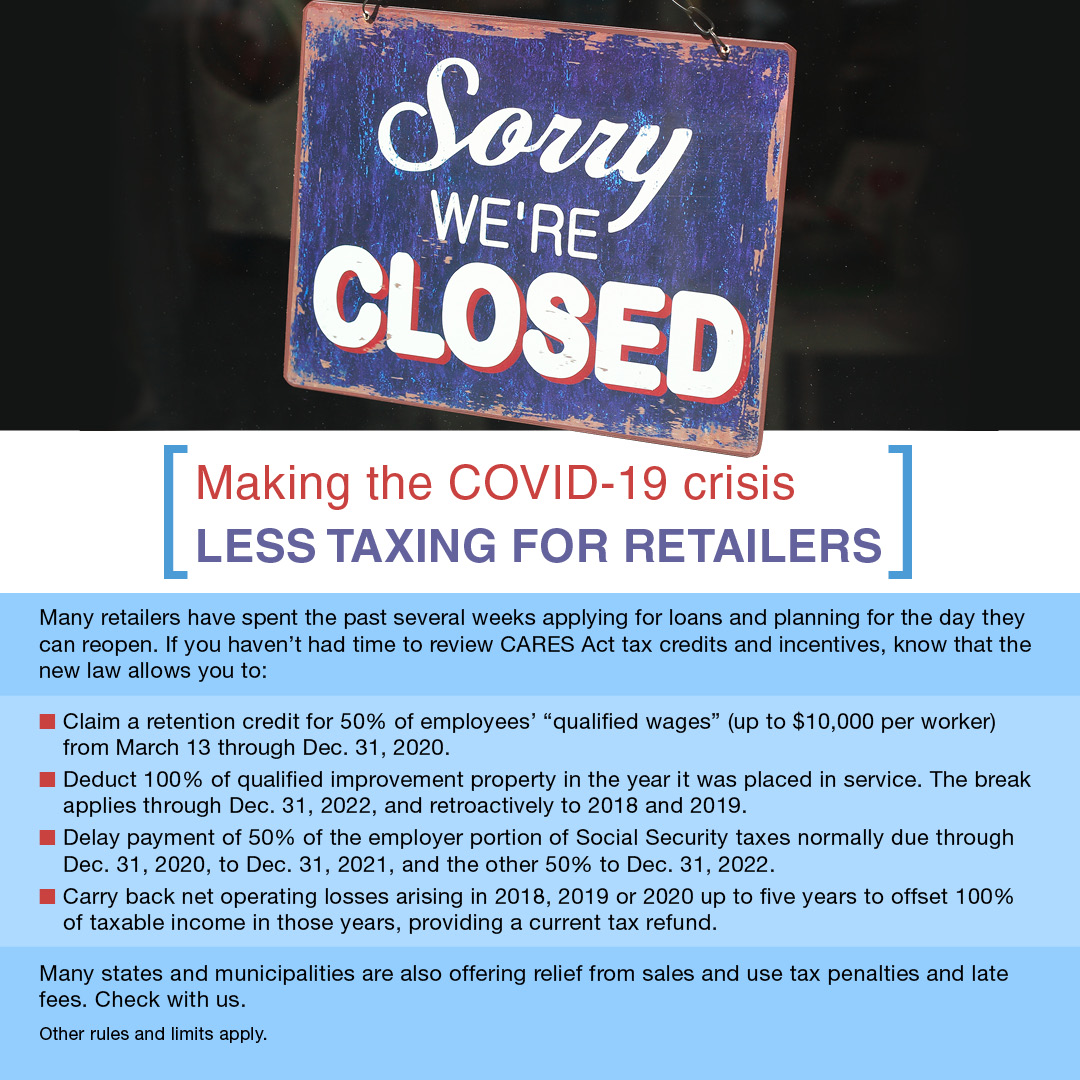

Making COVID-19 Less Taxing for Retailers

(This is Blog Post #842)

(This is Blog Post #842)

The COVID-19 pandemic has opened the floodgates to scam artists attempting to profit from sick, anxious and financially vulnerable Americans. Frontline efforts to corral Coronavirus fraud are […]

In light of the novel coronavirus (COVID-19) pandemic, many businesses are interested in donating to charity. In order to incentivize charitable giving, […]

Do you want to save more for retirement on a tax-favored basis? If so, and if you qualify, you can make a 2019 IRA contribution for the […]

In a News Release (IR 2020-48), the IRS has provided a list of payment options available to taxpayers who need to […]

The IRS recently released the 2021 HSA inflation adjusted amounts.

Not all companies follow U.S. generally accepted accounting principles (GAAP). Many smaller businesses, for example, have adopted the AICPA’s Financial Reporting Framework for Small and Medium-Sized Entities […]

As you may have heard, the Coronavirus Aid, Relief and Economic Security (CARES) Act allows “qualified” people to take certain “coronavirus-related distributions” from their retirement plans without […]

The Coronavirus (COVID-19) pandemic has affected many Americans’ finances. Here are some COVID-19 individual tax questions answered.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act eliminates some of the tax-revenue-generating provisions included in a previous tax law. Here’s a look at how the […]