Ways Your Business Can Accelerate Taxable Income and Defer Deductions?

Typically, businesses want to delay recognition of taxable income into future years and accelerate deductions into the current year. But when is it prudent to do the […]

Typically, businesses want to delay recognition of taxable income into future years and accelerate deductions into the current year. But when is it prudent to do the […]

If your business doesn’t already have a retirement plan, now might be a good time to take the plunge. Current retirement plan rules allow for significant tax-deductible […]

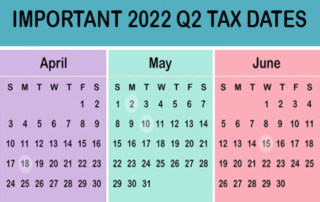

Here are some of the key tax-related deadlines that apply to businesses and other employers during the second quarter of 2022. Keep in mind that this list isn’t all-inclusive, […]

In today’s economy, many small businesses are strapped for cash. They may find it beneficial to barter or trade for goods and services instead of paying cash […]

The credit for increasing research activities, often referred to as the research and development (R&D) credit, is a valuable tax break available to eligible businesses. Claiming the […]

You may have wondered why, in a given year, you may be taxed on more S corporation income than was distributed to you from the S corporation in which […]

Back in 2017, the Tax Cuts and Jobs Act was signed into law which instituted a cap on the amount of state and local taxes (SALT) that individuals […]

If you own your own company and travel for business, you may wonder whether you can deduct the costs of having your spouse accompany […]

Do you want to withdraw cash from your closely held corporation at a minimum tax cost? The simplest way is to distribute cash as […]

If you’re in business for yourself as a sole proprietor, or you’re planning to start a business, you need to know about the tax […]