Work Opportunity Tax Credit Provides Help to Employers

In today’s tough job market and economy, the Work Opportunity Tax Credit (WOTC) may help employers. Many business owners are […]

In today’s tough job market and economy, the Work Opportunity Tax Credit (WOTC) may help employers. Many business owners are […]

Does your business need real estate to conduct operations? Or does it otherwise hold property and put the title in the name of the […]

Now that Labor Day has passed, it’s a good time to think about making moves that may help lower your small business taxes for […]

Do you own a successful small business with no employees and want to set up a retirement plan? Or do you want to upgrade from a SIMPLE […]

The business entity you choose can affect your taxes, your personal liability and other issues. A limited liability company (LLC) is somewhat of a […]

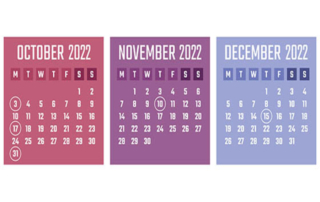

Here are some of the key tax-related deadlines affecting businesses and other employers during the fourth quarter of 2022. Keep in mind that this list isn’t all-inclusive, […]

The Inflation Reduction Act (IRA), signed into law by President Biden on August 16, contains many provisions related to climate, energy and taxes. There […]

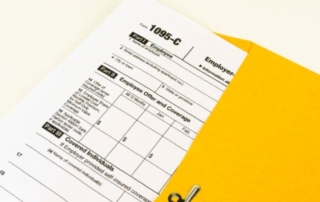

As you’re aware, certain employers are required to report information related to their employees’ health coverage. Does your business have to comply, and if so, what must […]

Sometimes, bigger isn’t better: Your small- or medium-sized business may be eligible for some tax breaks that aren’t available to larger businesses. Here are some examples.

These days, most businesses have websites. But surprisingly, the IRS hasn’t issued formal guidance on when website costs can be deducted.