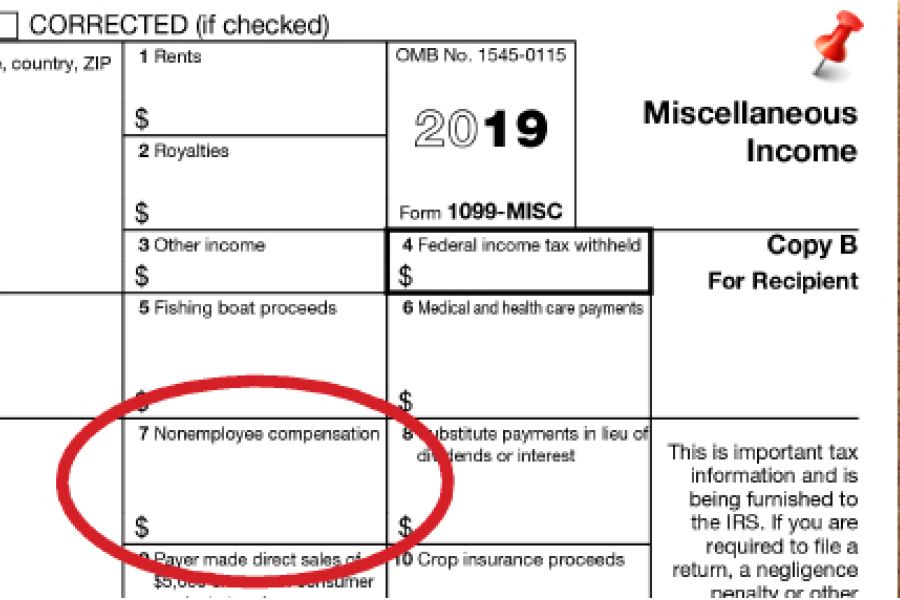

It's 2020, and with it your business may be required to comply with rules to report amounts paid to independent contractors, vendors and others. 1099-MISC reporting requirements may mean you have to send 1099-MISC forms to those whom you pay nonemployee compensation, as well as file copies with the IRS. This task can be time consuming and there are penalties for not complying, so it’s a good idea to begin gathering information early to help ensure smooth filing. Deadline There are many types of 1099 forms. For example, 1099-INT is sent out to report interest income and 1099-B is used to report broker transactions and barter exchanges. Employers must provide a Form 1099-MISC for nonemployee compensation by January 31, 2020, to each noncorporate service provider who was...